In 2026, Korea’s paper industry is taking pressure from four directions at once. The cost of pulp: the core raw material: has climbed back toward record territory. The won has weakened against the dollar, ocean freight rates have jumped, and a record antitrust fine landed in April. Each pressure on its own would be manageable. Combined, they are reshaping the industry’s outlook for the year.

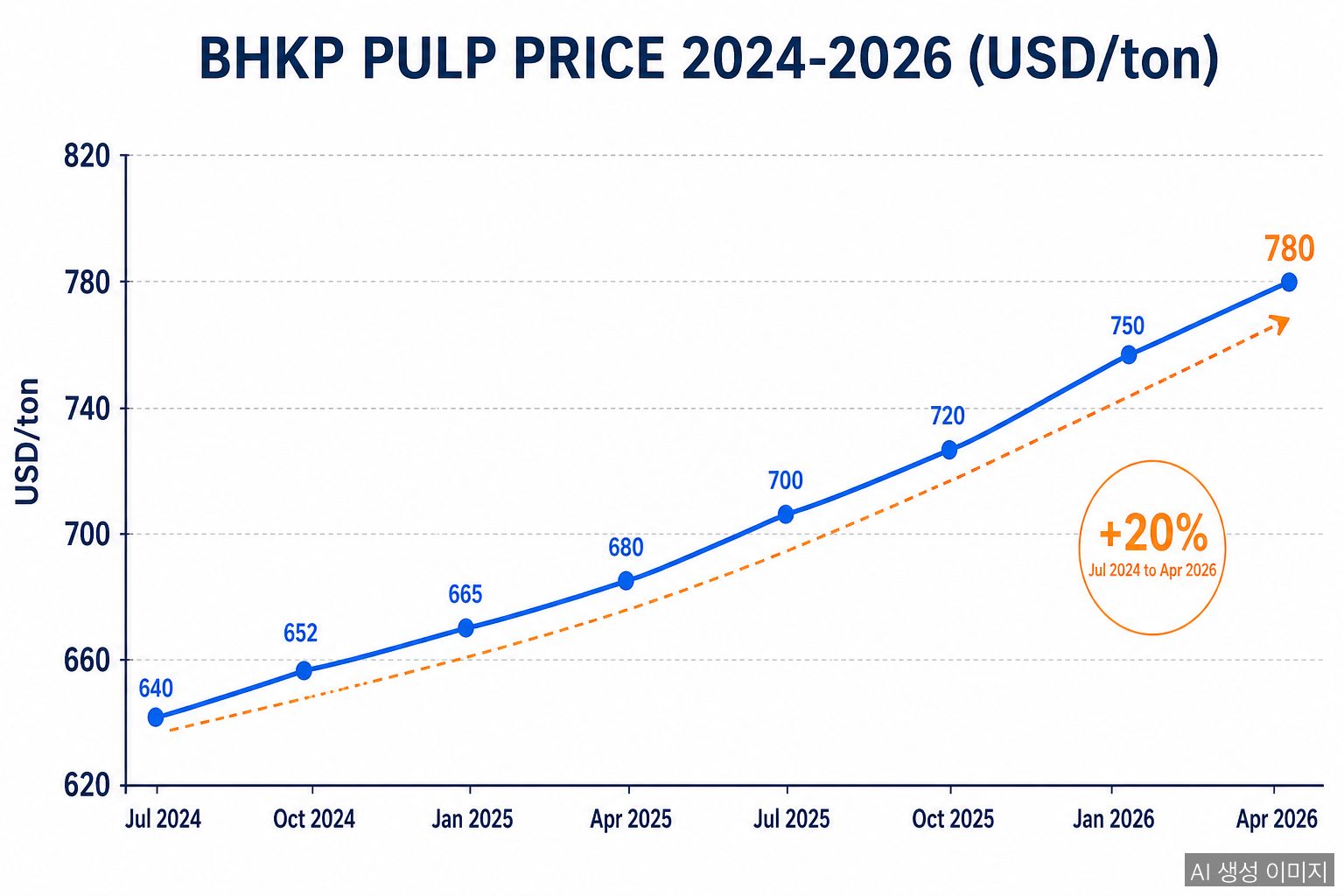

Pulp Prices: Up Over 20% in a Year

The benchmark Bleached Hardwood Kraft Pulp (BHKP / SBHK) traded at USD 780 per ton as of April 22, 2026: up 2.63% from March (USD 760). Compared to last July’s USD 640, prices are up more than 20%. Bleached Softwood Kraft Pulp (BSKP) is following a similar trajectory.

The drivers: tighter global supply discipline, recovering demand from China and India, and the structural shift toward paper-based eco-packaging.

Structural Vulnerability: Korea Imports Nearly All Its Pulp

Korea’s paper industry has a built-in exposure to pulp prices. With the partial exception of Moorim P&P, which sources some of its pulp internally, every other major Korean producer: Hansol Paper, Korea Paper, Hongwon Paper, and others: relies on imports for the bulk of its raw material.

Pulp typically accounts for more than 50% of the cost of printing and industrial paper grades. A USD 100/ton swing translates immediately to margin compression: there is no buffer.

₩1,500 Won, +30% Container Freight

The won has been hovering around ₩1,500 per dollar through April. Since pulp imports are dollar-denominated, every won decline raises the local-currency cost of the same shipment.

Ocean freight has joined the squeeze. The Shanghai Containerized Freight Index (SCFI) is up more than 30% versus pre–Middle East tension levels. Pulp is bulky and freight-sensitive, so shipping cost increases pass directly into landed material cost.

The April Hit: ₩338.3B Antitrust Fine

The decisive blow came on April 23, when Korea’s Fair Trade Commission imposed a combined ₩338.3 billion fine on six paper makers: Hansol Paper, Moorim P&P, Korea Paper, Moorim Paper, Hongwon Paper, and Moorim SP: for coordinating printing paper prices over a three-year, ten-month period (Feb 2021 – Dec 2024).

For an industry already pressed on raw material, currency, and freight, the fine adds a one-time cost that some observers expect will tip several producers into operating losses for 2026.

The Limits of Price Pass-Through

In normal times, the textbook response would be price pass-through. In 2026 it is not that simple. Right after a high-profile antitrust ruling, raising prices is politically and reputationally fraught. The Fair Trade Commission has issued an explicit price-redetermination order. Downstream industries: printing, publishing, food: are pushing back.

Alternative levers being discussed include:

- Higher-margin eco-packaging (paper-based plastic substitutes)

- Export expansion (especially EU markets where eco-certification is a moat)

- Energy efficiency and on-site generation (cushion electricity costs)

- Long-term pulp contracts (hedge spot-price volatility)

Short-Term Outlook

International pulp prices are expected to keep climbing through Q2 2026. Currency stability depends on US Federal Reserve policy and the trajectory of Middle East tensions: neither of which suggests near-term relief. Korea’s paper industry is moving into a period where survival depends on absorbing external shocks while restructuring at the same time.

FAQ

Q: Why does a pulp price increase hit Korean paper makers harder?

With the partial exception of Moorim P&P, which sources some pulp internally, every other major Korean producer relies entirely on imports. Global price moves pass into local cost without delay or buffer.

Q: What share of paper manufacturing cost does pulp represent?

For printing and industrial paper grades, pulp accounts for more than 50% of the cost. A USD 100/ton swing translates directly to margin movement: there is no cushion.

Q: How does FX affect pulp prices for Korean buyers?

Pulp imports are priced and settled in US dollars. With the won at around ₩1,500/USD, the same shipment costs significantly more in won terms: combining material price increases with currency depreciation as a double hit.

About the Author

PackingMaster: Editor of PaperPackLog. Covers market trends, product insights, and technology in the paper packaging industry.

References